When discussing commodities, most investors first think of crude oil, natural gas, gold, silver, wheat, or rare earth minerals. However, many people are surprised to hear that the world's second largest commodity market is actually iron ore. Iron ore is the main ingredient in steel and is used to create a wide variety of products, including steel coil that is used in cars and machinery, steel pipe used in the oil and gas industry, and steel beams and rivets used in construction. Despite its ubiquitous nature, steel garnered relatively little attention until 2010, when the world's major iron ore miners banded together.

The majority of the world's seaborne iron ore is controlled by three producers who control approximately 75% of the market. The seaborne iron ore market is where the majority of the world's iron ore is traded (see picture below). The big three include Vale in Brazil (VALE), BHP Billiton (BHP) and Rio Tinto (RIO) in Australia. The three miners' majority control over the seaborne iron ore market makes them formidable price setters and has allowed them to squeeze their customers.

For over 100 years, iron ore was bought and sold on an annual contract basis. This makes sense since iron ore is typically used to make steel, and steel is often used for large projects that take months or years to complete. Therefore it was beneficial for a steel producer to have a set price, and then pass on that set price to their customers. This pricing system seemed set in stone until March of 2010, when the big three teamed up and forced steel producers to move from an annual contract to a quarterly price contract.

click to enlarge images

(Source: Reuters.com)

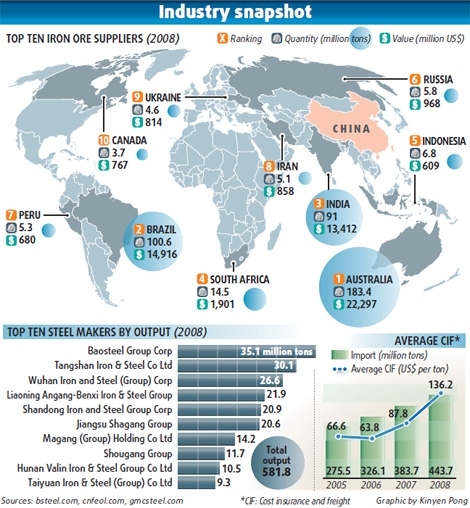

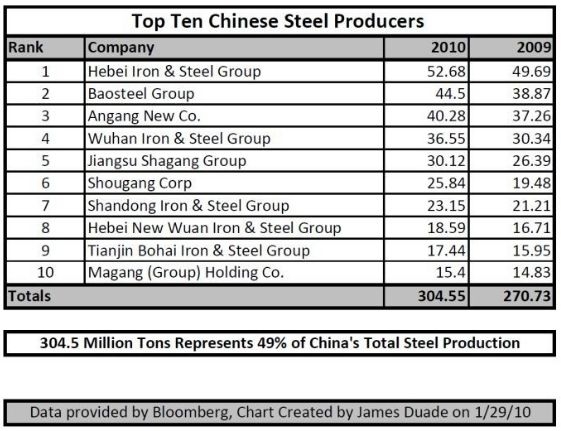

The big three are able to squeeze their customers largely because their major customer, China, has a historically fractured steel industry. The fractured nature of the steel industry forces these customers to take the spot price of whatever the market will bear. As the charts below illustrate, world consumption of iron ore is on the rise, and China is by far the largest importer. The second chart illustrates that there is no single dominant player. In fact, there are ten firms that constitute approximately half of China's steel output.

(Source: SteelOrbis.com)

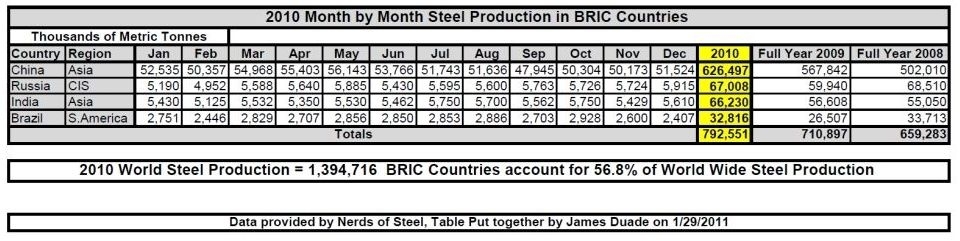

In 2010, world steel production reached a new record high of approximately 1.4 billion tons, the majority of which was produced in China and other emerging markets. This trend is likely to continue, as emerging markets begin to develop and require more and more infrastructure projects in order to meet the demands of their citizens for buildings, pipelines, or consumer products like cars and household appliances. This emerging market demand recently led Rio Tinto CEO Tom Albanese to predict that iron ore demand for his firm would double in 15 years.

An additional factor driving the price of iron ore higher is the move from the annual pricing contracts to the quarterly pricing contracts. This move has significant implications for the price of iron ore. Before the move to the quarterly contracts, iron ore was the world's largest commodity market without a spot price or a derivatives market. The annual pricing mechanism effectively meant that steel companies had no real need to hedge their purchases. However, with a move to quarterly contracts, a real need has arisen, and an emergent derivatives marketstarted to form earlier this year.

Derivatives, quite simply, are financial products that derive their price from an underlying product, which in this case is iron ore. The derivative can take many forms; for instance, you can have a swap where a steel producer would hedge their iron ore purchases at a certain price with a partner who would take the other side of the bet. In this instance, the steel producer would have a set price for iron ore purchases for a defined time period, and the swap partner would have to pay or be paid the difference between the set price and the actual spot price. In addition to swaps, other financial products like ETFs and futures contracts would increase the liquidity of iron ore, and allow the commodity to have a much greater presence than it already has.

Furthermore, increased demand for the underlying commodity can cause the price of the commodity to go up. This phenomenon has caused a spike in a variety of commodities like oil (OIL), silver (SLV), and gold (GLD). Overall, the extra liquidity provided by derivatives and other financial instruments provides investors and industry insiders greater opportunities to participate in the iron ore market.

An additional factor that impacts iron ore markets, as well as commodity markets as a whole, is the recent weak dollar policy. Iron ore, like all commodities, is priced in the world reserve currency, which of course is the U.S. dollar. The relationship is not always perfect, but generally, as the U.S. dollar strengthens, its ability to purchase good increases, which in turn makes the price of those goods less valuable. Conversely, when the value of the dollar decreases it can purchase fewer goods, and the price of those good increase. While quantitative easing has not led to a large increase in the CPI, it has led to a bull market in commodities that isn't likely to stop until a more hawkish stance on the dollar occurs. Lastly, it should be noted that, generally, as the value of the dollar decreases, the value of other currencies is strengthened in relative terms.

The Chinese renminbi over the last several years has been pegged to the U.S. dollar. This peg positively impacts Chinese exporters as they can provide a stable price to their customers in other countries, but particularly in Europe and the United States. Recently, the Chinese have discussed slowly removing this peg. If this were to happen, China would likely see an immediate increase in the renminbi relative to the dollar, which would in effect allow them to import commodities, which are priced in U.S. dollars, at a cheaper rate. As the previous tables describe, this is important for iron ore exporters because China is by far the world's largest importer of iron ore.

Many companies are poised to profit from a bullish iron ore market. As previously discussed, the dominant global players are the big three: Rio Tinto, BHP Billiton, and Vale. Other players in the industry include South Africa's Kumba Iron Ore (KIROY.PK), and the dominant player in the North America Cliffs Natural Resources (CLF). Additionally, several smaller Canadian firms would provide exposure to the iron ore market as well, including New Millennium Capital (NWLNF.PK), and Labrador Iron Mines (LBRMF.PK). Lastly, an iron ore royalty trust in Minnesota called the Mesabi Trust (MSB) would also provide excellent exposure to the iron ore industry.

Further Reading

No comments:

Post a Comment