Recently I published two articles (Iron Ore and Other Asset Bubbles andWhy I'd Avoid Iron Ore at Current Levels) highlighting some risks around the iron ore market. In this article, I will highlight some potential catalysts that can pop this bubble.

The logical reasoning behind the iron rally is the new demand created by emerging market infrastructure projects. In my view, this argument has been overplayed and if you check the recent iron price rally, the importance of Chinese demand is becoming less significant and the influx of money from the developed world under the QE plans is becoming more significant.

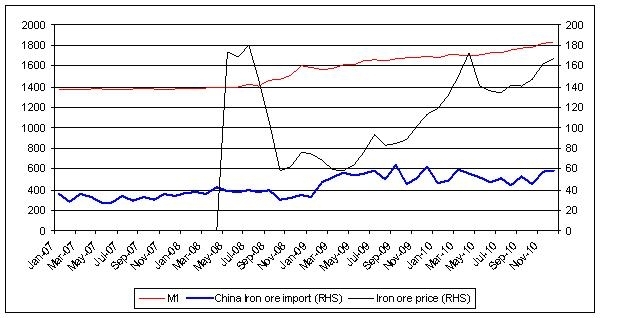

Chart 1: Recent iron ore price movements have more to do with U.S. money supply than China iron ore imports.

Click to enlarge

Correlation of iron ore with U.S. money supply has increased recently.

I checked the correlation among the three lines in chart 1 during two periods. First period is from 31/Oct/2008 to 30/June/2010 and then the second period is from 31/July/2010 to 31/Dec/2010.

I have summarized the correlation in these two periods below:

Table 1: Correlation among Iron prices and U.S. money supply is increasing.

Iron ore price vs. Chinese imports | Chinese imports vs U.S. money supply | |

31/Oct/2008 to 30/June/2010 | 0.26 | 0.06 |

31/July/2010 to 31/Dec/2010 | 0.03 | 0.55 |

31/Oct/2008 to 31/Dec/2010 | 0.24 | 0.10 |

As the table clearly shows, toward the end of the year, U.S. money supply had more to do with iron ore prices as more and more people crowded into the space with extra cash.

Potential catalysts that can pop the bubble:

- A slowdown in demand from China.

In my view, inflation and the other asset bubbles that are being created are becoming a bigger problem in China than the underdeveloped infrastructure.

In another year or two there will be a massive growth in the iron ore supply due to all the capex programs from mining companies. Hence it makes sense for China - and India - to delay development projects by about a year or two to benefit from these capacity expansions. This way they don’t have to pay astronomically high iron prices for their projects. After all, Chinese people have been living with current underdeveloped infrastructure for several years and a one-year delay won’t make a huge difference.

But if inflation raises, it is going to have a sudden impact on the lifestyle of the people and will put more pressure on the ruling party. This will make the Chinese government more inclined to slow down the growth in the short term for the greater benefit in the longer term. They have already raised short term interest rates and a few more rate hikes should slow down the demand for new iron ore demand.

- U.S. money supply slows down after June 2011.

The U.S. economy is showing early signs of a recovery and if this trend continues there is a very high possibility for the Fed to end current QE programs. As we can see in chart 1 and table 1, the money supply from U.S. was helping iron ore prices and under a scenario, such as the Fed ending its QE plans, iron ore prices can weaken.

The ending of QE policy should also see less downward pressure on the USD. Since the iron price is quoted in USD, an appreciating USD will also drag the quoted iron ore prices.

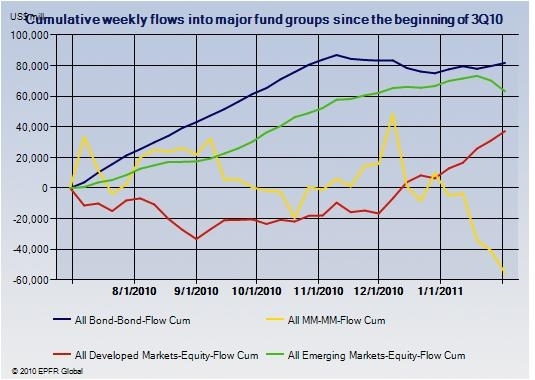

- With a recovery in developed markets, investors are moving out of emerging markets.

Based on a recent publication by EPFR fund flow data service, it seems investors have already started to take money out of emerging markets, in February 2011. A continuation of this trend would suggest the money supply in developing markets will slow down as well.

One reason for the recent iron ore price rally was that investors were left with large amounts of cash but without any quality investment options. But if investors start to see a recovery in the U.S. economy they will take money out from the iron ore market. After all if you have made a 200%-plus return you want to lock some profit from your investment.

Chart 2: investors moving back to developed markets.

Click to enlarge

4. Increasing capacity will create an oversupply scenario.

As I mentioned in my previous article, mining companies are increasing capacity at an unprecedented rate.

- BHP (BHP) in its half-year results announced a capex program of U.S. $80bn within the next 5 years. Just to get an idea, from 2005 to 2010, BHP spent only U.S. $ 48bn in capex projects.

- Rio Tinto (RIO) in its FY10 results announced that it wants to increase iron ore production by 50%.

Unlike copper, iron ore is not a very rare mineral. If the prices remain at current levels more and more projects will come online increasing the supply levels.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Please contact me at msoreff@seekingalpha.com regarding Seeking Alpha's Premium Content.

ReplyDeleteThank you!

Matana Soreff